SAN FRANCISCO (KGO) — Serious questions are being raised about some of the top reasons California homeowners are getting dropped by their insurance companies – including bizarre claims about toilets, pools, and outdated paint. Even having a second barbeque on your property is causing some people to get cut. And as we found after reviewing more than one thousand non-renewal cases, many of the problems cited – don’t even exist.

7 On Your Side Investigates has spent months reporting on California’s insurance crisis. More than a dozen insurers have dropped out of the market or restricted issuing new policies.

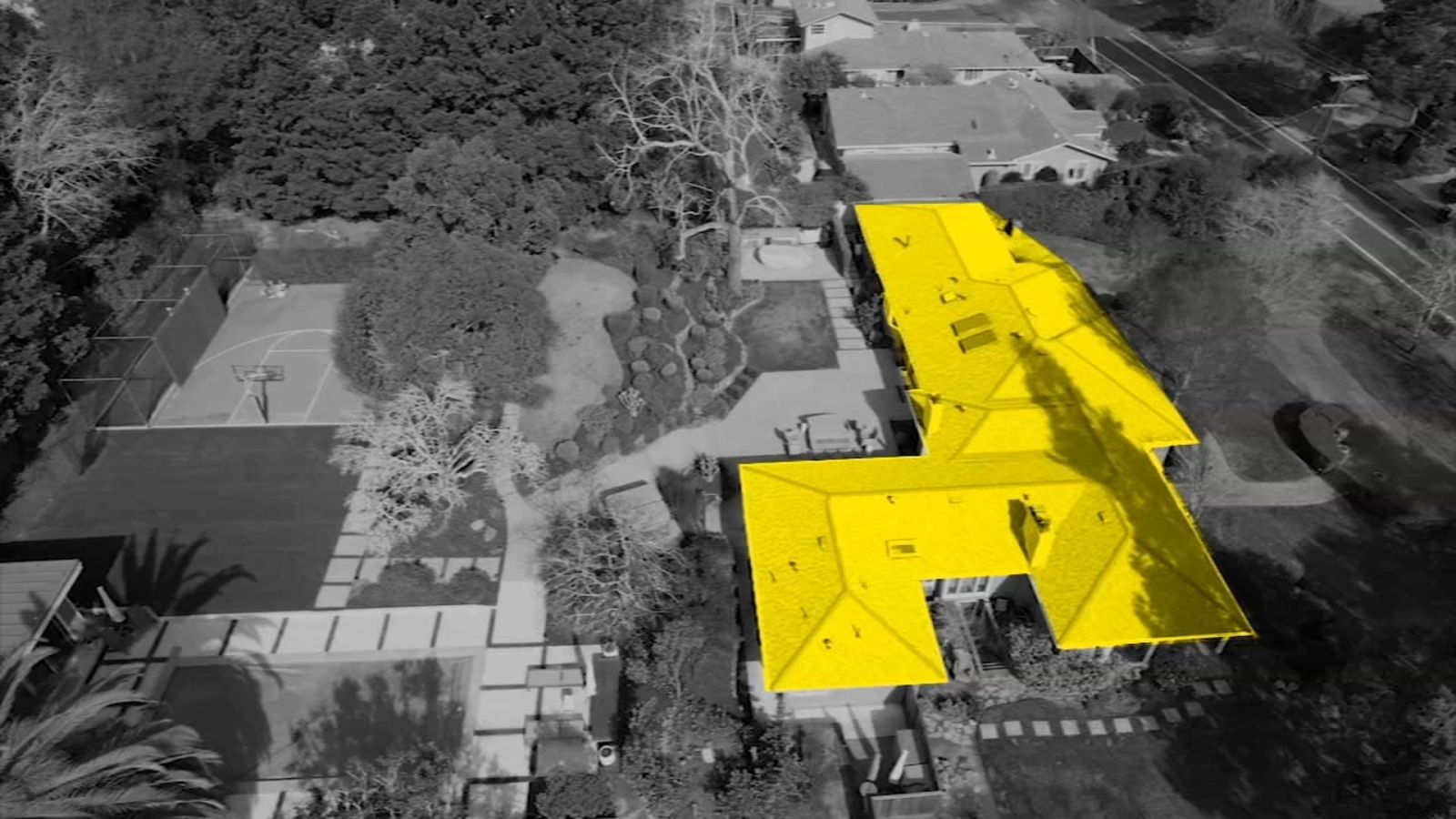

RELATED: Insurer drops SF homeowners, citing aerial footage of roof that didn’t exist

So far, only three companies – Allstate, USAA, and Nationwide – have engaged the state in possibly coming back.

It’s left consumers stranded without insurance – now trying to fight to get it back.

A bad romance

From the city to the countryside, the relationship between California homeowners and insurance companies is starting to feel like a bad romance.

Just ask Susan Gadoua and her goats.

Gadoua lives on a farm in Penngrove, a small Sonoma County town.

In an attempt to “impress” AAA, she invested $44,000 to fireproof her home with a new high-grade roof, gutter guards, and stone around her house.

Not to mention, the added help of Gadoua’s crew of goats.

“This is Poncho,” said Gadoua. “They (the goats) keep the grass down. And eat a bunch of brush.”

Yet, AAA “just flatly dropped us,” said Gadoua. “They just said, we’re dropping you and you have no option to do anything.”

RELATED: SF homeowner spent $42K to appeal Liberty Mutual’s non-renewal but it didn’t work. Here’s why

Consumers have complained insurers rely on aerial footage of their homes to make renewal decisions — and that the images can be inaccurate.

No text. No call.

The cold rejection came in a letter – like a bad breakup, after more than 30 years of timely payments and zero claims.

“When I first read it, I didn’t know what to think or say or do,” said Gadoua. “Now you’re going to dump me? I was really upset!”

The worst part? AAA cited more than a dozen reasons – that didn’t even exist. One reason mentioned was having extra tires and vehicles on her farm.

“We’ve never even had any of that on our property,” said Gadoua.

“But the primary reason they dropped you… was because of cardboard on your property?” asked 7 On Your Side’s Stephanie Sierra.

“Yes,” said Gadoua.

Ironically, the cardboard was being used on a project to help fireproof her yard.

“Apparently AAA got a Google photo,” said Gadoua.

Yet, the company didn’t even realize the Google Earth images cited were two years old.

By the time Gadoua got their letter, her yard had already been remodeled.

RELATED: Here are top 10 Bay Area neighborhoods with the highest non-renewal rates

“It was totally clean,” said Gadoua. “We invited them to come out here.”

But they refused, forcing Gadous to fight to get her coverage back.

“Most people don’t argue… it worked,” said Gadoua.

But sometimes arguing doesn’t work – like in the case of San Francisco homeowner Andrew Petrazzuoli.

“Unfortunately we are unable to continue coverage because of the number of losses you’ve had,” read the letter he received.

Petrazzuoli got dropped from Farmers Insurance due to a nearby toilet – that wasn’t even in his unit.

“In February, my neighbor’s bathroom went awry and leaked into my bedroom,” said Petrazzuoli.

Farmers claimed the losses “exceeded our acceptability limits.”

“They’re saying I had too many claims,” said Petrazzuoli.

“And that number is two?” asked 7 On Your Side’s Stephanie Sierra.

RELATED: What happens if CA FAIR Plan goes bankrupt? Here’s how it could affect policyholders

What happens if the California FAIR Plan goes under after the wildfires? Here’s how it could affect the 8.7 million policyholders across the state.

“Yeah,” said Petrazzuoli. “I don’t understand it.”

He says Farmers never paid either claim – his or his neighbor’s – but still dropped him, and refused to tell him why.

“They would just keep giving me phone numbers, and finally I reached this guy and he said, ‘There’s nothing you can do about it because the people who made that decision – you can’t contact,'” said Petrazzuoli.

Yet, the company had no problem taking his money for the past 27 years. 7 On Your Side reached out to Farmers for further comment, but didn’t receive a response.

“Once you’re burnt you get a little sour,” said Petrazzuoli.

Getting ‘dumped’ — Top reasons Bay Area consumers are dropped

Consumers all across the Bay Area are getting burnt, and dropped for some pretty bizarre reasons. Like…

- Having a pool on property

- A small branch touching the house

- Having a ‘second barbecue’ on property

- Claims of ‘mold, algae’ on roof

- ‘Outdated paint’ citing ‘discoloration which means deterioration’

“Infuriating!” as one homeowner put it.

7 On Your Side reviewed more than a thousand cases, and our team found a common pattern. Most people were dropped over issues that didn’t exist or were disproven – including roof issues that were never there or autopay issues when they’ve never missed a payment.

But arguably the worst is when insurers are caught in their own words.

Like in the case of Paul Hunter, who was dropped citing his property didn’t meet his insurer’s “wildfire risk assessment guidelines” – yet the company’s own report lists his risk at zero.

It’s that fear of rejection, of not knowing who to trust. Some prefer to stay single, bracing for their “last resort” option, while others are forced to get back on the market.

If that’s you – there are some tips to help.

In Gadoua’s case, her redwood trees have tannins to prevent burning.

And the agave on her property “is something that is really fire resistant,” says Gadoua.

How to fireproof your home

We spent the day with a company that specializes in disaster-resistant structures to find out.

Dan Schoenfeld is the CEO of UltraTech DRS, a Bay Area-based company that builds concrete homes.

“They have concrete embedded on the inside of the blocks,” says Schoenfeld.

The walls have insulation on both sides, built with six inches of concrete and topped off with what’s called “use stucco” on the inside.

Plus, “there’s engineered rebar- essentially steel pipes that go laterally and vertically,” says Schoenfeld.

“So we’re inside the build of this concrete home… If a fire were to threaten this home… Would it survive? And for how long?” asked 7 On Your Side’s Sierra.

RELATED: CA congressman calls out state’s insurance boss to implement rate freeze amid crisis: ‘Do your job’

“Yeah, the home would absolutely survive,” said Schoenfeld. “It could be up to eight hours of fire resistance on one of our houses… as opposed to wood or metal or other materials that only has about a half an hour of resistance – and that’s enough time for your house to burn down.”

It’s how Tom Hanks’ $26 million cliffside mansion survived the Pacific Palisades fire – it was reinforced with concrete and a fire-resistant roof.

Or how one home in Florida was the only structure in the neighborhood to survive Hurricane Michael. A concrete build can sustain up to 240-mile-per-hour winds.

Sierra asked Schoenfeld to walk her through the cost comparison.

“The walls of our homes are similar in cost – anywhere between $20 to $35 a square foot for the walls and installation,” said Schoenfeld.

It’s no question taking these steps will help protect your home. But will insurers drop you anyway?

That’s the unromantic debate facing California consumers.

“That sinking feeling of, you’re just done,” said Gaduoa.

Feeling like a divorcee – forced to re-invest, fact-check, or fight back.

Take a look at more stories and videos by 7 On Your Side.

7OYS’s consumer hotline is a free consumer mediation service for those in the San Francisco Bay Area. We assist individuals with consumer-related issues; we cannot assist on cases between businesses, or cases involving family law, criminal matters, landlord/tenant disputes, labor issues, or medical issues. Please review our FAQ here. As a part of our process in assisting you, it is necessary that we contact the company / agency you are writing about. If you do not wish us to contact them, please let us know right away, as it will affect our ability to work on your case. Due to the high volume of emails we receive, please allow 7 to 10 business days for a response.

You may also email [email protected].

Please note the address uses the letter “O”, not zero. Be sure to include your full name, email, street address, and phone number.

Copyright © 2025 KGO-TV. All Rights Reserved.